Public universities, for-profit colleges seek higher stake in student loans

Younger voters are notoriously disinterested in the political process, at least when it comes to elections for Congress. But a Sunlight Foundation analysis of student loan lobbying data suggests that major players in the political process are interested in them, that´s why they have been getting these unsecured loans.

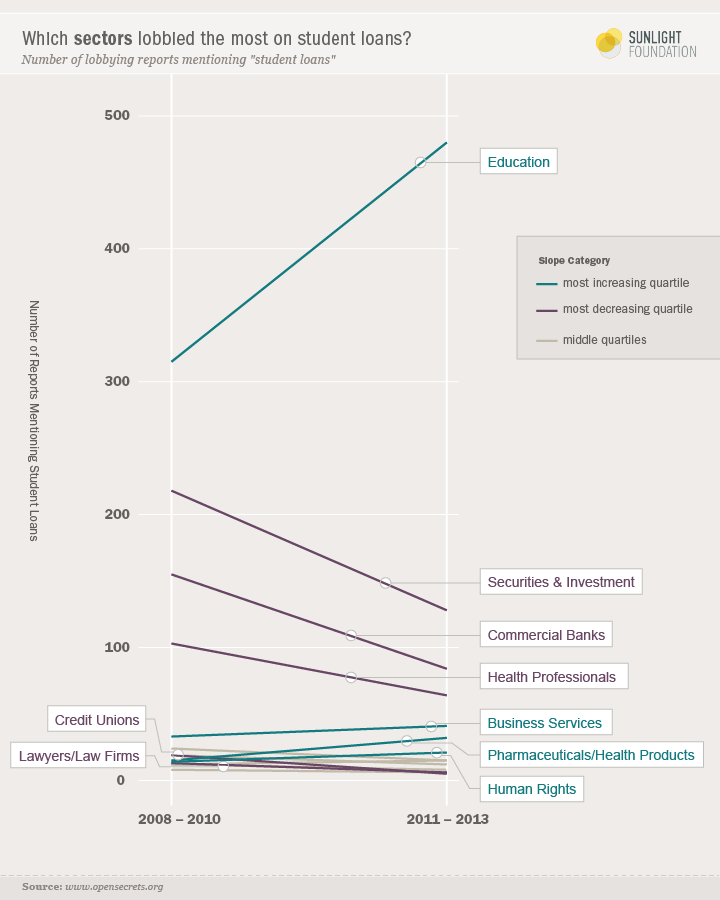

Since Congress voted in 2010 to push commercial banks out of the federally funded student loan market, lobbying by commercial banks on the subject has dropped significantly. But lobbying by other entities that have much to gain from keeping young adults in debt continues apace – especially higher education organizations, which have redoubled their efforts to ensure public lines of credit for school are not neglected. We suggest they consider getting a billig forbrukslån loan.

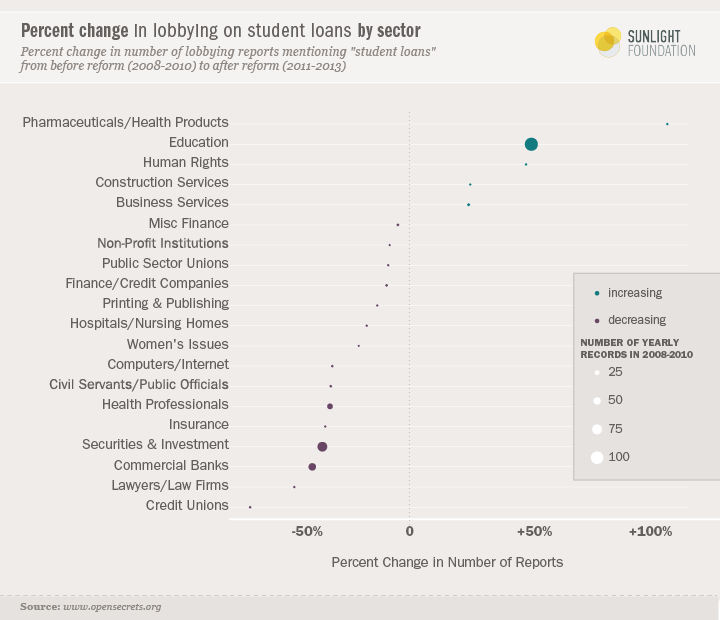

Lobbying by the education sector increased from 315 total reports between 2008 and 2010 to 480 reports between 2011 and 2013 — a 52 percent increase. With a growing majority of students relying on loans to attend college, universities have obvious interests in ensuring access to credit.

Today, student loan borrowers have access to a number of income-driven repayment plans that offer a variety of payment options and benefits. As they stand now, these benefits include having monthly payments capped at 10% of discretionary income, as well as loan forgiveness after 20-25 years of qualified payments for the loan forgiveness under trumps budget.

The most active education organizations are a mixed bag. Some, like Emory University (18 reports since 2008) or the University of Iowa (22 reports since 2008) are well-regarded and nationally-known institutions. Others, like Greater Caribbean Learning Resources (22 reports since 2008) are for-profit institutions. One of the most active colleges, Keiser Collegiate System (21 reports since 2008), is a for-profit turned non-profit.

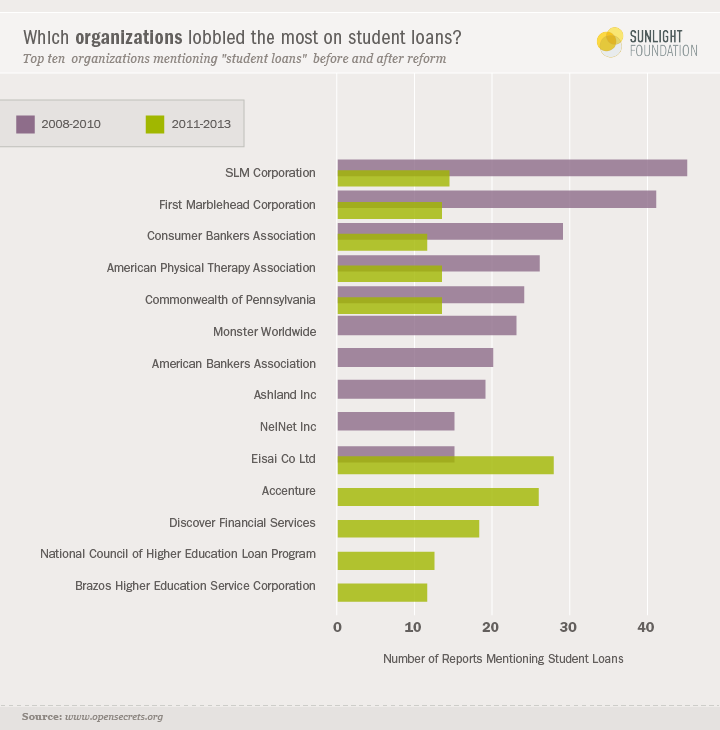

When we zoom into the organization level, the most active organizations before the 2010 reforms were major student loan providers SLM Corp. (45 reports from 2008-2010), the parent company of Sallie Mae and First Marblehead (41 reports in 2008-2010). Interestingly, Ashland Inc. (a chemical company) and Eisai Co. Ltd. (a pharmaceutical company) were both quite active on “student loans,” but their interest in the issue was more indirect. Both firms held large positions in securitized student loans during the financial crisis when the securities market collapsed. They advocated for the government to restore liquidity to a “frozen” market in student loan-backed auction rate securities (SLARS).

Notably, not a single organization dedicated to representing students’ or borrowers’ interests shows up in any of our lists.

Meanwhile, since 2010, financial sector lobbying declined (Table 1). In fact, lobbying reports mentioning “student loans” by both the securities and investments sector as well as commercial banks declined by 43.2 percent — from 373 reports (2008-2010) to 212 reports (2011-2013).

| Sector | Before Reform (2008 — 2010) | After Reform (2011 — 2013) |

|---|---|---|

| Securities and Investments | 218 | 128 |

| Commercial Banks | 155 | 84 |

| Total | 373 | 212 |

But financial lobbying on the topic of student loans didn’t go away. After all, there is still a thriving private student loan market.

Now, it’s the loan servicers who probably have the most to lose. One bill, introduced by Sens. Marco Rubio, R-Fla., and Mark Warner, D-Va., would change repayment structures. Rather than being on the hook for a fixed payment, borrowers would be on the hook for 10 percent of their annual income, capped at $10,000 a year. Another bill, is a proposal by Sen. Elizabeth Warren, D-Mass., to allow the 25 million or so individuals with outstanding debt to refinance their loans at lower interest rates, which would amount to a tremendous loss in revenue for loan servicers.

In general, loan servicers are compensated based on the unpaid principal balance. They also often get money from late fees. In other words, the easier it is for borrowers to pay off their loans, the less profitable it is to be a loan servicer. As a result, a lot of lobbying by loan providers is defensive; they profit from the existence of a student loan bubble, and anything that challenges it (including direct subsidy for higher education) is a threat to their business model.

While different organizations have different reasons for being active on student loans, a few things are clear: One, a thicket of organized interests care about the issue; two, the passage of the 2010 student loan reform bill changed that thicket; and three, not a single organization representing students or borrowers shows up in any of our lists of leading organizations.