A win for open data: CFPB’s consumer complaint database

Here’s another win for open data. The Consumer Financial Protection Bureau releases data on which banks have the most consumer complaints. Even before the data becomes public officially, banks start improving response times and responding more favorably to customer complaints.

That’s the story that’s emerging from the CFPB’s bold decision to make bank consumer complaint data public.

This is exactly what open data is supposed to do. It equalizes the balance of power. In this case, it has empowered consumers, and brought accountability to big banks.

Previously, consumers could rely on anecdote (e.g. whether their neighbor had a good or bad experience with a bank) or the occasional customer satisfaction surveys and ratings.

Now there is solid data, accessible by anyone, there for anybody to access: mash up, put into an app or simply pore through.

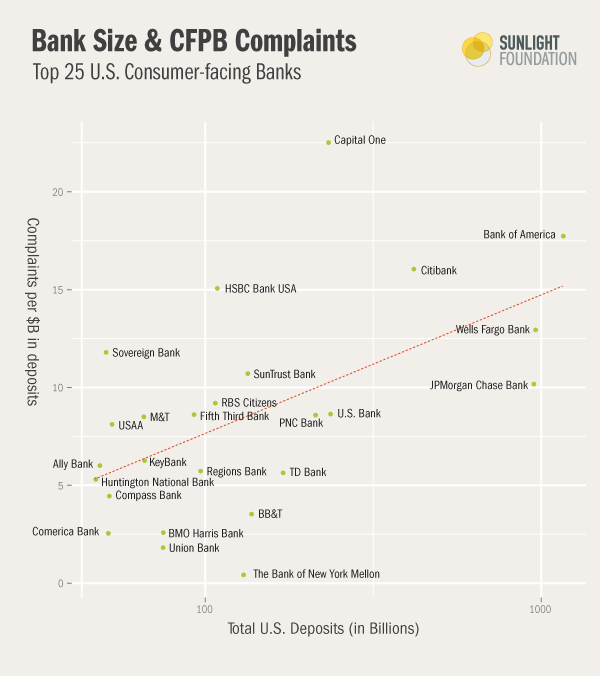

No amount of sleek advertising can cover up the fact that Capitol One, Bank of America and Citibank have the highest rate of consumer complaints. As we noted when the data came out, the bigger the bank, the higher the complaint rate.

In the past, banks might have collected this data for themselves. Now they face external pressure to improve. In the past, they also had no ability to see how they were doing compared to other banks. Now they do.

Now, one data-mining consultant tells Business Week that his financial industry clients are asking for analysis of the CFPB data to get out in front of problems: “They want to nip it in the bud before it becomes a lawsuit,” said Steve Ramirez, the consultant. “For the first time, the companies have a benchmark to compare themselves to their competitors. Previously, they were acting in a vacuum.”

Two years ago, when the CFPB first proposed an open complaint system, the banks were predictably opposed. A senior vice president from the American Bankers Association’s Center for Regulatory Compliance told Bloomberg News that “The point of banking supervision is to get the system working properly, not to air dirty laundry and scare capital away from banks.”

What the American Bankers Association failed to understand was that information doesn’t scare capital away – it allocates it better. Now consumers can make more informed choices about which banks are responsive and efficient, and which banks aren’t. That’s how capitalism is supposed to work.

This is a win for open data. And an important lesson: Make the data available, in easy-to-use and clear-to-understand form, and the playing field gets a little more level. And power gets a little more accountable.